Introduction

The blockchain is a new way to think about managing data and transactions. It’s a public ledger that records every transaction ever made on it; this makes the blockchain transparent, secure, and hard to tamper with.

What is blockchain?

Blockchain is a shared database, or ledger, that’s stored on multiple computers around the world. It has many different applications but is most commonly used to track transactions and payments.

Blockchain technology uses cryptography to create an immutable record of transactions that cannot be altered by any individual or organization without the consensus of all parties involved in those transactions. This makes it secure against fraudsters who would seek to manipulate data for personal gain–and also ensures transparency in financial dealings between businesses and individuals alike.

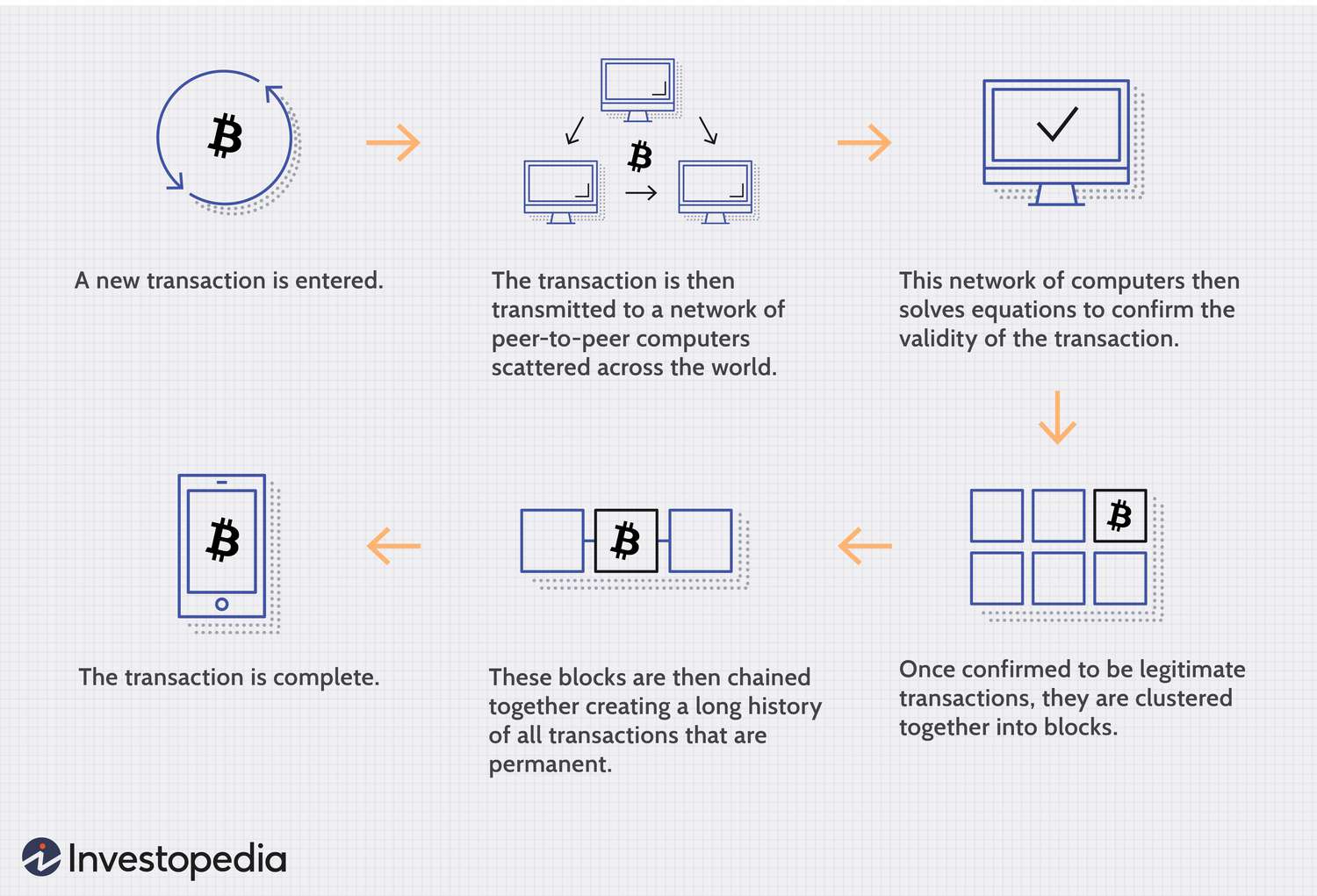

How does blockchain work?

How does blockchain work?

Blockchain is a decentralized system for storing data. It’s made up of blocks and transactions, which are stored across a network of computers called nodes. Each node has its own copy of the blockchain, but they don’t connect directly with one another–instead, they communicate through shared protocols (for example: TCP/IP). This means that no single entity controls all the information in the blockchain or can tamper with it without being detected by other users in the system.

Why does blockchain matter?

Blockchain is a secure and transparent way to record transactions. It’s decentralized, meaning that there is no central authority controlling the system, and it allows for peer-to-peer transactions that are recorded on a public ledger. The public ledger is immutable and cannot be changed; once something has been recorded in the blockchain, it stays there forever–therefore making it incredibly tamperproof.

Blockchain allows users to engage in financial transactions without the need for middlemen such as banks or brokers (who traditionally take fees). The technology also eliminates any risk of fraud because every transaction made with cryptocurrency is verified by multiple nodes within milliseconds before being added into what’s known as “blocks” within the chain itself–and those blocks cannot be altered at all!

How does blockchain apply to healthcare?

Blockchain technology can be used to store and share data in a secure way. This is important for healthcare because patient records are often scattered across different institutions, making it difficult to access information when it’s needed most.

Blockchain also helps track the provenance of drugs and medical devices, which could help prevent counterfeit drugs from entering the supply chain.

Another use case for blockchain is tracking patient consent: if you’re going into surgery tomorrow morning, your doctor may want your permission before using something like an MRI machine on you–but how do they know if they have permission? With blockchain-powered systems like MedRec (which was developed at MIT), every time someone grants permission or denies access during their visit with a doctor or nurse practitioner (or even just visits a website), those changes get recorded automatically so there’s no question about what happened later down the road when someone else needs access

How can you start using blockchain technology?

If you’re interested in learning more about how blockchain technology works and how it can be used to create new opportunities for businesses and individuals alike, there are many resources available. The first step is understanding what blockchains are, what they’re capable of doing and where they’re headed as a whole. Once you understand the basics of this emerging field, you’ll be ready to explore ways in which your own business might benefit from incorporating them into its operations.

The public ledger can be used by banks, health care companies, and more.

The public ledger is a database that’s shared among many different people. It’s called “public” because anyone can access it, and it cannot be changed or removed by any single party.

The use cases for blockchain technology are endless–from tracking diamonds to helping you find your lost phone. But one of the most promising uses is in banking and finance, where it can be used to track payments between parties more efficiently than traditional systems do today (and with fewer fees).

Conclusion

Blockchain technology is a game changer in the world of healthcare. It has the potential to streamline processes, improve data security and transparency, and even save lives. But what does this mean for you? If your company is looking to use blockchain technology, we’re here to help!